The largest aluminum producer in the world, Alcoa Inc. (NYSE: AA) outperformed analyst consensus estimates for the first quarter of 2011. Alcoa announced earnings after the market closed on Monday.

And yet, the company’s stock price dropped more than 5% yesterday.

To be honest, I’m not extremely interested in Alcoa’s quarterly earnings report, or any other company’s earnings report either.

I’m far more interested in the fact that Alcoa sold off after announcing a 1 penny earnings outperformance. At the same time, Alcoa’s revenues came up short of expectations.

Typically, when a company sells off after it beats earnings estimates, it’s a sign of a top for either the company in general, or if it’s a bellwether like Alcoa, it could signal a top in the markets.

Why is Alcoa a bellwether? They’re traditionally the first company to report during earnings season every quarter. Obviously, Alcoa’s earnings won’t bleed into IBM’s (NYSE: IBM) earnings – but the market’s reaction to such earnings could.

The fact that Alcoa’s earnings beat expectations but their revenues came up short also suggests that the earnings growth could be signaling cost-cutting or jiggering the books instead of real growth. You can’t fake sales very easily – but earnings can be adjusted and reworked a hundred different ways.

So what’s going on with revenues?

For one, the company’s $5.96 billion Q1 sales tell us that it pays to be a commodity producer these days.

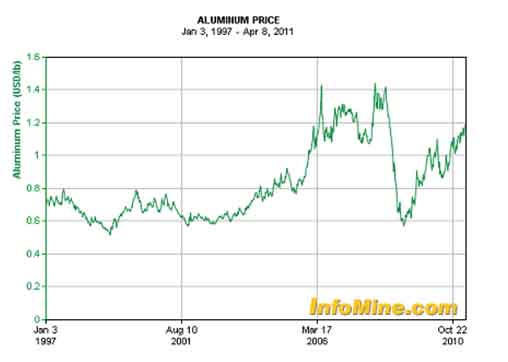

That’s a 22% increase over their sales in Q1 of 2010. And if you take a quick look at the chart of aluminum prices below, you can see why.

Aluminum prices climbed about 11% between April 2010 and today, so the fact that Alcoa was able to increase sales by twice that amount should tell you about their ability to capitalize on higher aluminum prices.

Except for the 2006-2008 period, aluminum prices are at modern record highs. Even accounting for that period, they’re only 16% from those highs.

I don’t like to buy anything when it’s selling at or near all-time highs and it seems as though the market sentiment is coming around to that same conclusion.

Also, aluminum prices are tied heavily to growth. No one buys bricks of aluminum during a currency crisis. It’s a vital component in all types of construction, manufacturing, and industry growth.

Additionally, or perhaps, most importantly, aluminum prices are practically welded to the prices of energy commodities such as oil.

Take a look at the chart below which plots oil (in red) vs. the Dow Jones US Aluminum Index (in black).

I think if you believe in the Chinese growth story and/or you believe that the global recovery will be a sustained one, then you should look for any dips in Alcoa’s prices as a buying opportunity.

If you believe that growth will slow in China, and that the recovery will be short lived, you should look to sell Alcoa.

But in any event, you should be aware of the likelihood of continued short-term price movement that’s based entirely on market sentiment.

If you’ve been holding on to Alcoa and waiting for this earnings announcement, you might look at a lack of strength in the stock price and the revenues as a time to dump shares. After all, if a company can’t get a quick boost after it beats earnings, when will it rise in price? I’m not saying that’s a good ownership strategy, I’m just saying that many investors might have such an outlook.

That’s the type of market we’re in right now. Investors are clamoring to sell any kind of news, good or bad. They’ll use the news as a reason to get out of stocks they perceive as having climbed too high, too quickly.