Rio Tinto has agreed to sell its stake in the Simandou iron ore project in Guinea to partner Chinalco, setting the stage for a sizeable new competitor.

Rio will receive between $US1.1 billion and $US1.3 billion ($A1.4 billion to $A1.7 billion) for its nearly 47 per cent ,based on the timing of the development of the project.

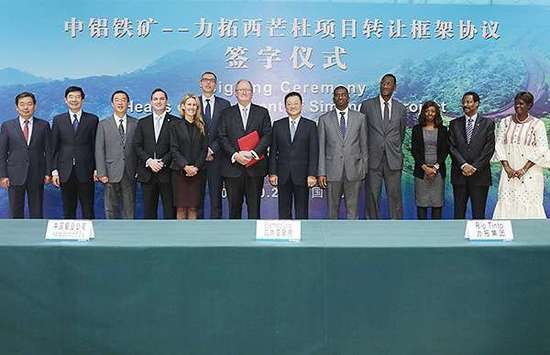

The company says it has signed an initial agreement with the Chinese state miner setting out the principal terms of the sale, and aims to sign a binding agreement within six months.

The iron ore giant announced in July it had decided to shelve development of the project - the world's biggest untapped deposit of iron ore - saying the enormous cost could not be justified given the huge overcapacity in the iron ore market.

Plans for the project included an iron ore mine in central Guinea, a 650-kilometre railway and a deepwater port on the West African country's Atlantic Coast.

The Aluminum Corporation of China, also known as Chinalco, already owns 41 per cent of Simandou. The Guinea government holds a 7.5 per cent stake.

Analysts previously have warned that an expansionist Chinese investor taking over the asset would leave Rio and larger rival BHP Billiton facing a sizeable new competitor in the global iron ore market.

Despite signs of a slowing economy, China remains the biggest market for the steel making ingredient.

Global mining majors, under pressure to maintain profitability amid an extended slump in commodities prices, have recently moved away from their strategy of pumping iron ore volumes to drive away smaller, higher-cost rivals, and are instead favouring other commodities such as copper and petroleum.

Rio, which in August posted its weakest underlying profit in more than a decade, has already pared back its 2017 guidance for iron ore shipments by up to five per cent.